One of the biggest questions I’m hearing right now from buyers across Greater Phoenix is simple:

“If the Federal Reserve is cutting rates, why are 30-year mortgages still hovering in the high-5% to low-6% range?”

It feels counterintuitive. For years, consumers were conditioned to believe that when the Fed cuts rates, mortgage rates automatically follow. But in reality, that relationship is indirect and often weak.

Here’s the core truth:

The Federal Reserve does not set mortgage rates.

Long-term investors do.

Understanding that difference can prevent costly timing mistakes, especially for buyers waiting for a dramatic drop that may never come.

What the Federal Reserve Actually Controls

The Fed’s primary tool is the Federal Funds Rate, the overnight rate at which banks lend reserves to one another.

That rate:

- Influences short-term borrowing

- Impacts credit cards and some adjustable-rate products

- Signals the direction of monetary policy

But it does not directly set:

- 10-year Treasury yields

- 30-year mortgage rates

- Long-term inflation expectations

- Investor appetite for risk

The Fed can influence market psychology, but it does not dictate long-term borrowing costs.

Mortgage Rates Follow the 10-Year Treasury, Not the Fed

Thirty-year mortgage rates move more closely with the 10-Year U.S. Treasury yield than with the Fed Funds Rate.

Why?

Most 30-year mortgages are packaged into mortgage-backed securities (MBS) and sold to long-term investors. Those investors compare mortgage bonds to Treasuries and demand a premium for additional risk.

Treasury yields move based on:

- Long-term inflation expectations

- Federal deficits and debt issuance

- Economic growth outlook

- Global capital flows

- Confidence in fiscal stability

Treasury rates reflect what investors think will happen over the next 10–30 years — not what the Fed did this month.

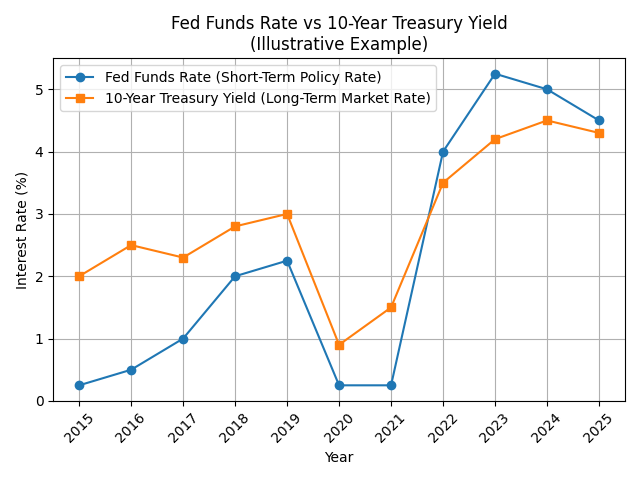

Fed Funds Rate vs 10-Year Treasury

(This chart illustrates how long-term yields often diverge from short-term Fed policy.)

How the 30-Year Mortgage Is Actually Priced

Here’s the simplified structure:

- A lender originates a mortgage.

- That mortgage is bundled into a mortgage-backed security (MBS).

- Investors purchase that bond and demand a yield.

Mortgage bonds carry additional risks beyond Treasuries:

- Inflation risk

- Duration risk (30 years is a long time)

- Prepayment risk (borrowers refinance when rates fall)

- Housing market and credit risk

Because of these risks, investors require a spread above Treasury yields.

When uncertainty rises, that spread widens, keeping mortgage rates elevated even if Treasury yields stabilize.

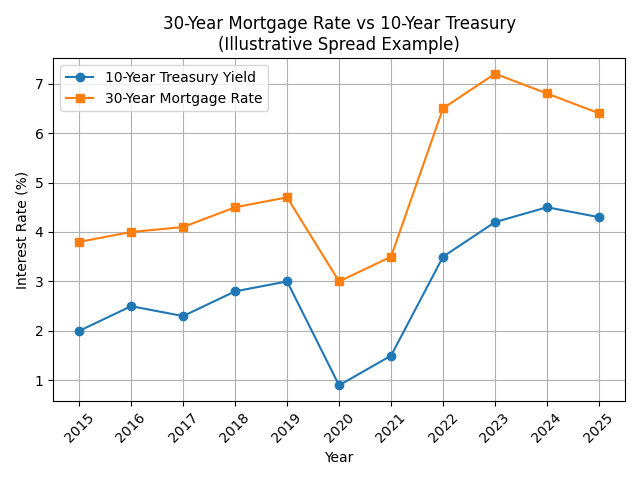

Mortgage Rate = 10-Year Treasury + Risk Spread

(This chart helps you understand why mortgage rates don’t fall 1-for-1 with Fed cuts.)

Why Today’s Environment Is Different From the Last 15 Years

Many buyers are anchored to the ultra-low-rate era following:

- The Great Recession

- Quantitative easing

- Pandemic-era bond buying

Those historically low mortgage rates were the result of extraordinary intervention, not normal market conditions.

Today’s backdrop looks different:

- Persistent federal deficits

- Heavy Treasury issuance

- Less aggressive central-bank bond buying

- Investors demanding real (inflation-adjusted) returns

Low 3% mortgage rates were an anomaly, not a long-term baseline.

What This Means for Buyers in Today’s Market

Waiting for Fed cuts alone to trigger dramatically lower mortgage rates may not be a winning strategy.

Rates may:

- Stay range-bound longer than expected

- Ease slowly rather than sharply

- Decline, but be offset by rising home prices

In markets like Scottsdale, Paradise Valley, and Greater Phoenix, inventory and price discipline matter more than trying to perfectly time rates.

Here’s the strategic shift:

**Negotiate price aggressively

**Buy the right property for long-term goals

**Understand refinance optionality

**Avoid paralysis based on outdated expectations

You can refinance at a rate.

You cannot renegotiate the purchase price.

Quick Reference Guide

| Fed Funds Rate | Federal Reserve | Overnight | Inflation & Employment Policy |

| 10-Year Treasury | Global bond market | 10 years | Growth, Deficits, Inflation Outlook |

| 30-Year Mortgage | MBS investors | 30 years | Treasury Yield + Risk Premium |

Bottom Line

Federal Reserve rate cuts do not automatically mean lower mortgage rates.

The 30-year mortgage reflects long-term economic expectations, not short-term policy shifts. Buyers waiting for a return to crisis-era rates may be waiting for something structurally unlikely under current fiscal and market conditions.

In today’s environment, success comes from focusing on value, negotiation, and long-term ownership strategy, not headline timing.